The most expensive retirement mistake may not be picking the wrong fund or failing to predict the market. It may be waiting—telling yourself you will start after the next raise, after the debt is gone or when life feels more settled.

That delay can look harmless because the skipped deposits seem small. But the real loss is not only the money you did not contribute. It is the growth that money could have earned, plus the growth on that growth, over decades.

This is the unforgiving arithmetic of compounding: time can do more of the work when you start early, and no strategy can buy back years that have already passed.

The short answer

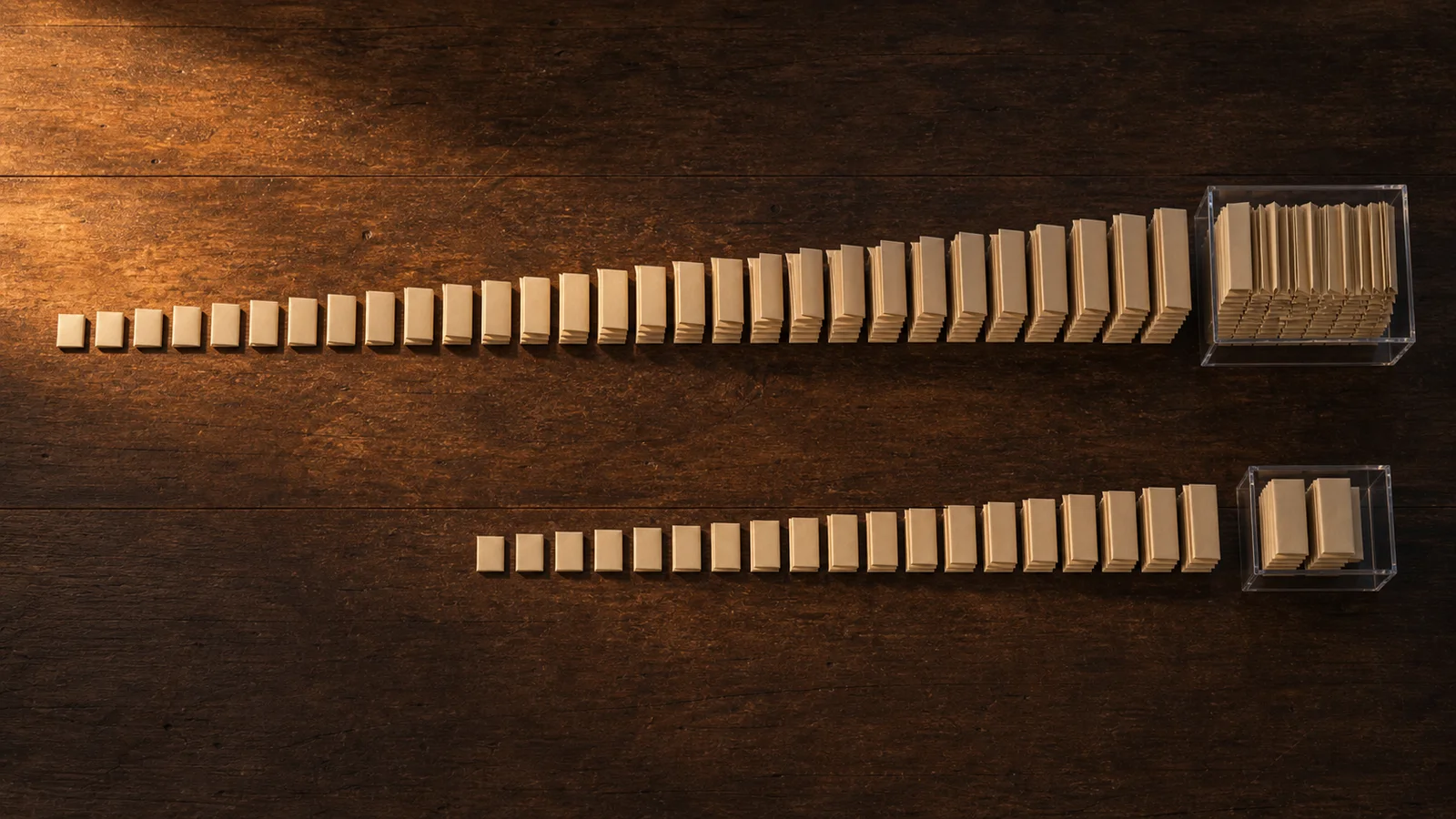

Consider two hypothetical workers who both invest $500 a month and earn an average 7% annual return, compounded monthly. One starts at 25 and continues until 65. The other waits until 35 and also stops at 65.

The early starter would contribute $240,000 over 40 years and finish with about $1.31 million. The later starter would contribute $180,000 over 30 years and finish with about $610,000. The 10-year delay creates a gap of roughly $702,000—even though the difference in out-of-pocket contributions is only $60,000.

Those numbers are an illustration, not a promise. Markets do not return the same amount every year, and taxes, investment fees and inflation affect what a future balance can buy. The point is the scale of the time advantage. The Securities and Exchange Commission's Investor.gov compound-interest calculator lets readers test different contribution amounts, time periods and estimated rates.

How waiting turns into a six-figure problem

Compound growth means returns can generate additional returns. In the first years, the account may appear to move slowly because the balance is small. Later, the same percentage return applies to a much larger base, so growth can accelerate.

That is why the final decade in the 40-year example is so powerful. A person who starts later does not merely miss 10 years at the beginning. They also reach the final years with a much smaller balance available to compound.

The Department of Labor's Saving Matters guidance urges workers to begin the habit early, even with small amounts, because starting sooner can reduce how much they need to save later.

The second loss: money your employer might have added

If a workplace retirement plan offers matching contributions, waiting or contributing below the match threshold can deepen the damage. The IRS explains that employees generally must participate and contribute from their salary to receive a match, with the formula and eligibility rules set by the plan.

Imagine an employer that adds 50 cents for every dollar an employee contributes, up to a stated limit. An employee who waits is not only missing their own investment and its potential growth; they may also be giving up employer money and decades of potential growth on that money. Check the plan's summary description for the exact formula and vesting rules rather than assuming every match works the same way.

Do this first

- Start with an amount you can sustain. A smaller automatic contribution now is more useful than an ambitious plan that remains postponed. If $500 is unrealistic, test $25, $50 or 1% of pay.

- Capture the full employer match if your budget allows. Review the contribution threshold, enrollment instructions and vesting schedule in your plan documents.

- Automate the decision. Payroll deductions or recurring transfers remove the need to choose again every month.

- Raise the contribution gradually. Consider increasing it after a raise, when a recurring bill ends or on a fixed annual date.

- Review investment costs and diversification. Starting early helps, but high fees or a concentrated portfolio can introduce avoidable risk.

If you started late, the answer is not panic

The calculation is meant to show the value of acting, not to shame anyone. Many people delay because of low wages, caregiving, medical costs, housing expenses or high-interest debt. Starting later still leaves time for growth, and a realistic plan is better than freezing in regret.

Begin by learning what you already have: old workplace accounts, a current employer plan, an IRA or a pension benefit. Then estimate the gap between your current path and your retirement goal. A larger contribution, a longer working timeline, lower expenses or a combination of changes may help, but each choice has different costs.

Common mistakes to avoid

- Waiting until debt is completely gone. High-interest debt often deserves priority, but some workers can still contribute enough to receive an employer match while paying debt down.

- Assuming a future raise will solve everything. Expenses often rise with income. An automatic percentage increase turns the intention into a rule.

- Chasing unusually high returns to catch up. Taking excessive risk can create a second problem. A higher assumed return is not a guaranteed shortcut.

- Treating the example as a forecast. A 7% average is a planning assumption. Actual results will vary, and future dollars will have less purchasing power than dollars today.

What to check this week

Open your most recent pay statement and retirement-plan portal. Confirm your current contribution percentage, employer-match formula, investment selection, fees and beneficiary information. If you are not enrolled, find the smallest automatic amount that fits your cash flow and identify a date to increase it.

For personalized guidance—especially when taxes, pensions, inherited accounts, major debt or retirement withdrawals are involved—consider a qualified financial or tax professional. General examples cannot account for your full situation.

The painful part of compounding is that lost time cannot be recovered. The hopeful part is that the clock starts helping as soon as you begin.